Bonds, stocks and cryptocurrencies can be a useful addition to close your own pension gap. Some apps make it particularly easy to get started with these forms of private old-age provision.

Thinking about your own retirement is definitely not one of the most pleasant activities. At least not when it comes to financial security. The topic is more urgent than ever, because those who are currently working will probably only be able to count on a basic state pension in the future, which by no means ensures the standard of living that has been maintained up to now. But there are now some really good apps that make it particularly easy to make private provision for your own future and increase your money. From our point of view, these interesting apps are worth a look.

Pension improvement apps

rubab

Behind the start-up “Rubarb” are Jakob and Fabian Scholz. Chancellor Olaf Scholz’s two nephews have developed an app that makes it particularly easy to save for retirement. Rubarb links to your current account, credit card or PayPal. Now, when shopping online or in stores, the sum of each purchase is rounded up to whole euros. The money collected then flows into a bond or stock portfolio ETF (Exchange Traded Fund).

You can choose between different security levels for the individual portfolios. The “Relax” portfolio contains only government and corporate bonds. These are generally safe investments. In the Discover model, the ratio between stocks and bonds is 50 percent each. The riskiest variant, “Challenge”, contains 100 percent shares. Depending on the portfolio selected, returns of 3.1 to 12.5 percent per year are given. ETFs are generally considered to be a relatively safe and simple form of investment, since you are not investing in the shares of a single company, but in an index such as the DAX or S&P 500. That is why they are also a good investment for retirement.

Also interesting: With these apps you keep your finances under control

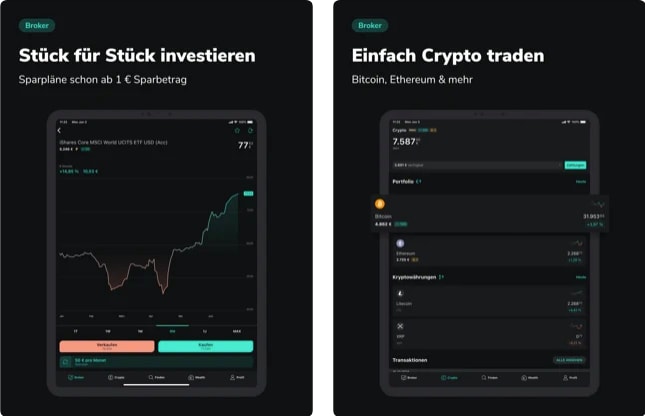

Scalable capital

Scalable Capital combines two pension options in one app. On the one hand, a “normal” broker where you can buy shares yourself. On the other hand, a so-called robo advisor; an algorithm that automatically invests the invested money in the capital market and thus promises the highest possible returns even to investors without stock market experience. Scalable Capital is one of the so-called “neo brokers” whose interface is specially designed for use on smartphones. In this way, stock trading should be greatly simplified and entry made easier.

Buying shares with Scalable Capital is comparatively cheap, so you only pay EUR 0.99 per transaction in the “Free Broker” model. Trading in ETFs and cryptocurrencies is also possible, but you don’t buy “real” coins here, but so-called Exchange Traded Products (ETP). These merely reflect the performance of the cryptocurrency and secure it.

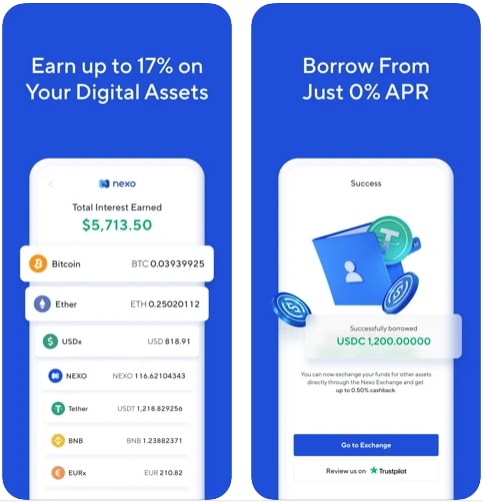

NEXO

Cryptocurrencies such as Bitcoin, Ether and Cardano are considered riskier investments compared to stocks, real estate or gold. On the other hand, they promise a comparatively high return, which in extreme cases can even reach more than 100 percent of the capital invested. Nexo is a so-called lending platform. Lenders and borrowers gather on it, with the difference that the loans are not secured with money but with cryptocurrencies.

The Nexo crypto account is one of the best-known offers in the industry, where returns of up to 20 percent per year can currently be achieved. This is well above the ECB base rate and the interest rates offered by regular commercial banks. Cryptocurrencies can be a useful addition to the investment mix, but you should never invest all of your savings in Bitcoin & Co.

Beware of the Treasury

In principle, all of the apps mentioned here are well suited, depending on personal risk tolerance on the smartphone, to privately save money for old-age provision or, ideally, to significantly increase invested capital. Bonds are the safest, while cryptocurrencies are the riskiest.

Also interesting: Which app is the best to buy ETFs?

However, it is important to know that the tax office also wants to earn money from the money saved. In the case of shares, it is therefore important to create an exemption order via the broker. Anyone who makes a profit from the sale of cryptocurrencies must then declare this independently in their tax return. Crypto exchanges or platforms do not pay taxes to the tax authorities. If you are unsure here, it is better to consult a tax advisor, especially when starting out.