. The new American president Donald Trump is imposing a whirlwind of enormous import duties on friends and enemies. Inflation that turns out to be higher than expected. National debts that are spiraling further out of control. An ideological estrangement between allies Europe and the United States. also a huge acceleration of plans to implement artificial intelligence.

which is holding up well worldwide.

A professional investor might then think: inflation, uncertain policy and international instability: ! But someone else could just as easily conclude: buy shares! Because the economy continues to grow, corporate profits are at a good level and the technological breakthrough of AI promises good times. This year they were both right.

Hundreds of events in 2025 would each have generated a news cycle lasting weeks, if not months, in any other year. But this year they were often lost in the enormous mass of incidents, plans, decrees and developments that raged on.

And so one of the most telling trends on the financial markets ended up under the radar: gold and shares reached records. And they gave a contradictory signal to each other: avoid risk, so flee into gold; and take risks, invest yourself in shares. It’s like looking at a steep mountain wall. There: a struggling climber looking down anxiously.

Dominance of tech

The Bank for International Settlements (BIS), which provides services for the global national central banks, pointed out last week the remarkable trend of simultaneously avoiding and seeking risks, which is reflected in the prices of gold and shares. The BIS does not really draw conclusions. But there are hints.

In recent years, many private investors have gained access to investments in things that previously could be accessed by professionals, such as gold and other commodities. Through listed investment funds (exchange traded fundsETFs) they now have that option, and they are taking advantage of it. In addition, countries outside the US are stocking up on gold, led by China, which may signal distrust in the US dollar and a desire to be independent of America’s economic and monetary policies. This fits in with the global push for greater national or regional autonomy that is emerging everywhere now that the global economy is becoming a bleak place.

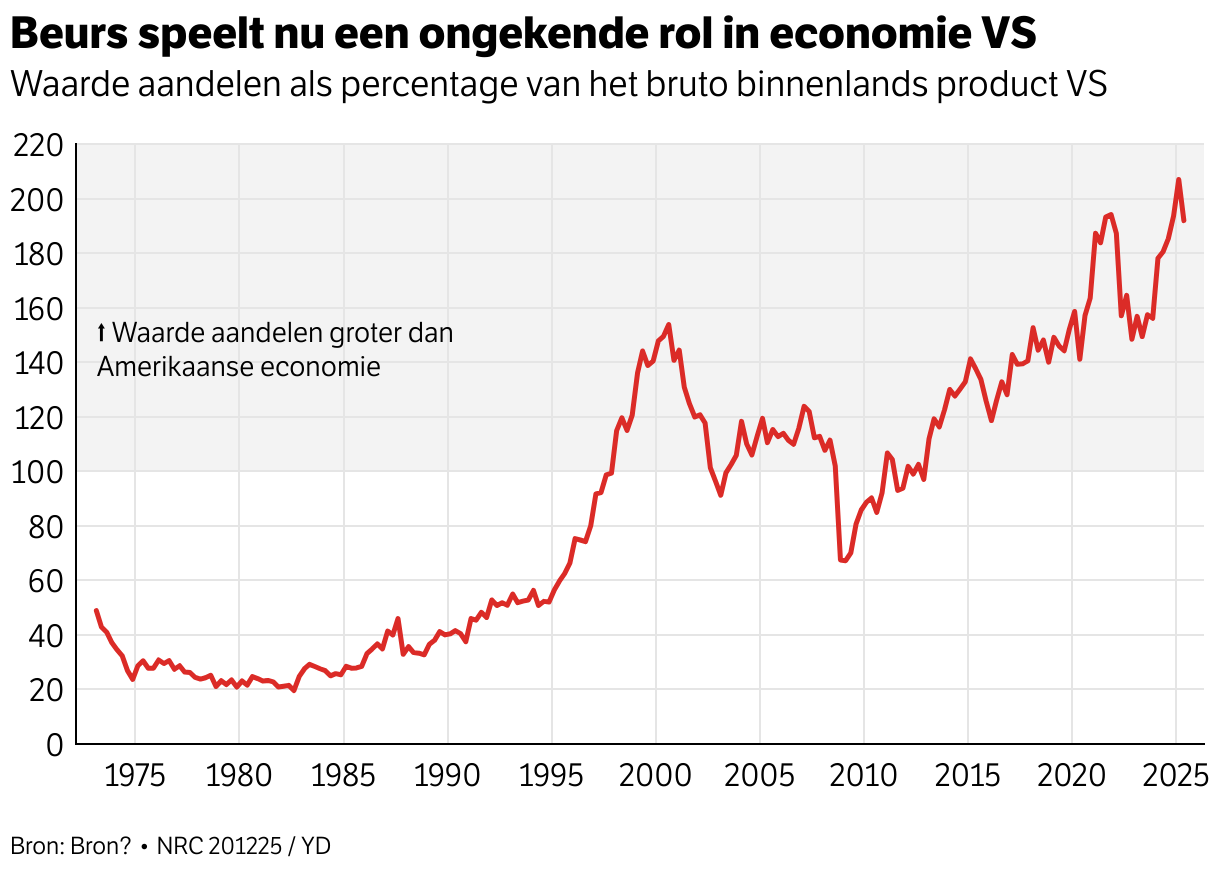

As for shares, prices are particularly high in the US, mainly due to the dominance of tech companies. Ten years ago, the so-called Magnificent Seven (Nvidia, Apple, Microsoft, Amazon, Meta, Alphabet and Tesla) were together worth 1,500 billion dollars on the stock market. Five years ago that was already 7,500 billion, at the beginning of last year it was 16,000 billion and by the end of this year they will be worth more than 19,000 billion dollars.

These are unimaginably high amounts, but when you compare them to the size of the American economy, you really see how fast things have gone. At the height of the dot-com bubble in 2000, all shares on the American stock exchange were worth one and a half times as much as the size of the American economy itself – the gross domestic product (GDP). This year the value rose to almost as much as US GDP – unprecedentedly large. For comparison: for the EU you should think of a total value of all shares that includes the entire European stock

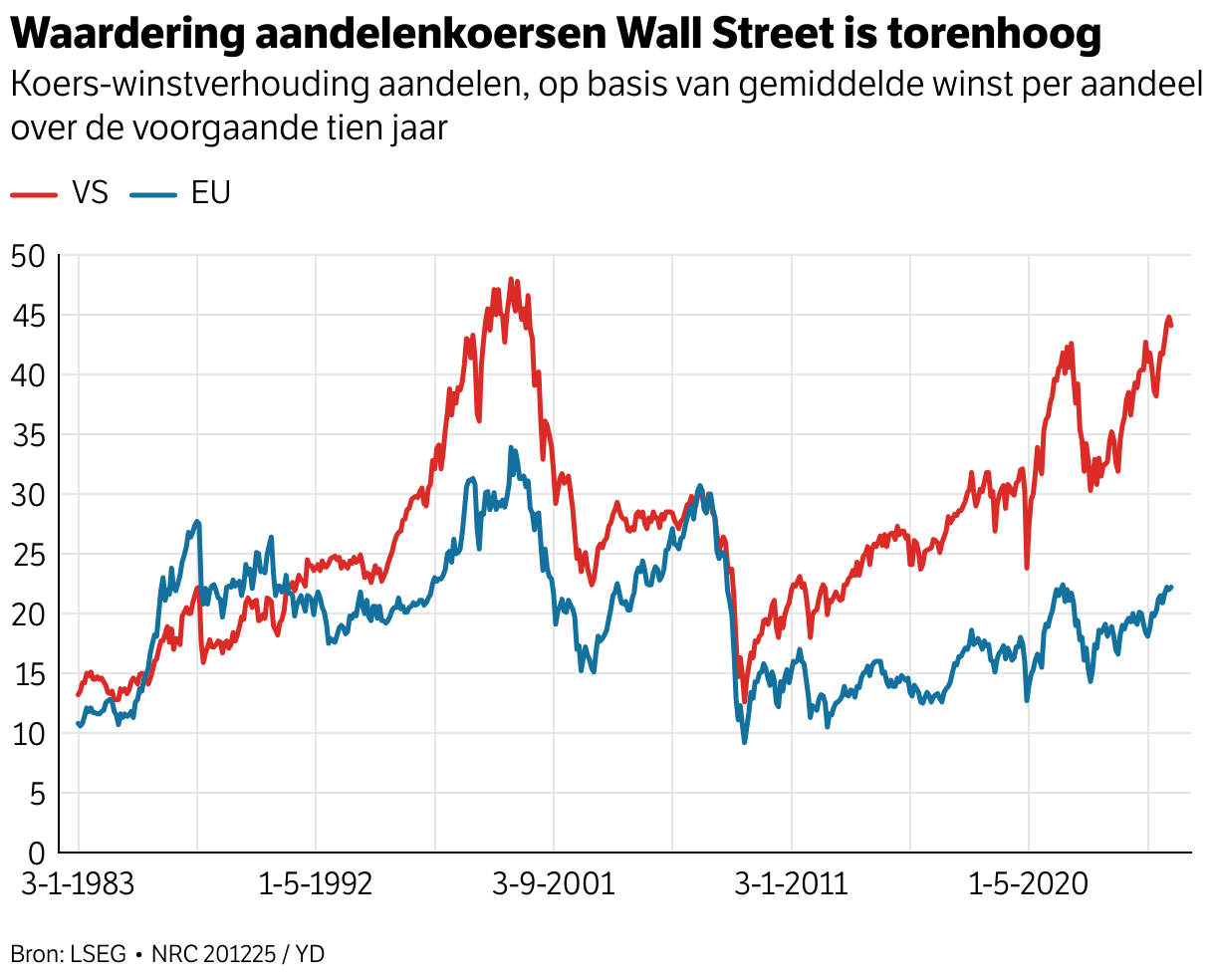

The level of American prices is also reflected in the valuation of shares: how many times the profit per share is paid for a share on average. Nobel Prize winner Robert Shiller became famous when he calculated this ‘price-earnings ratio’ in his own way in the late 1990s. He did not compare the price against the profit per share of the same year, but took the average profit over the last ten years. In this way he neutralized the influence of economic fluctuations to obtain a more structural representation of the stock market valuation. Shiller’s formula would have indicated long in advance that prices were difficult to maintain in those years. Anyone who uses his formula today arrives at an average stock market valuation that is almost as extreme as it was just before the bubble burst.

Paradoxical consumer

So the climber and the ibex are on a rather steep mountainside. But why do they deal with it so differently? For that answer you also have to look mainly at the United States, if only because that is where the most extreme economic policies take place. It is not only the financial markets that find themselves in a paradox of simultaneously seeking and avoiding risk. Such a contradiction also applies to consumers. Only 33 percent of Americans agree with Trump’s economic policy, according to the latest polls. But so far there is little evidence of this in their behavior. This discrepancy is also somewhat visible in the Netherlands. Consumer confidence is relatively low, depending on the behavior of those consumers.

The fact that the difference between thinking and doing is more extreme in the US is due to a major culprit: the increased cost of living. That may partly have to do with Trump’s policies. From April 1 this year, the president introduced significantly higher duties on American imports by decree. It depends a bit on how you calculate it, but right now the average levy is about 16 percent, up from just about 2.5 percent a year ago. Although importers do not pass on the bill for all or all of the increased import prices to their customers, the increased prices have contributed to inflation. Depending on the standard, it now amounts to about three percent. And consumers, just like in Europe, first experienced price increases after the corona pandemic and then those due to increased energy prices

what about the relatively high spending pattern of consumers? That is still unclear. But it may have to do with the promise of major economic stimulus, which at the same time is not entirely trusted.

Look at the One Big Beautiful BillTrump’s major budget intervention last year. It reduces taxes, especially for higher incomes, and cuts social spending on health care, food aid and student loan assistance. This will result in net additional expenditure of $3,400 billion over the next ten years.

And then there are the enormous expenditures that tech companies are making, and increasing, on artificial intelligence and the data centers that it requires. Estimates indicate that these alone will have led to 1.1 percent GDP growth by 2025. That is significant: it is slightly more than half of the total economic growth in the US over 2025. And the effect will continue for the time being as the rise continues.

The government therefore provides extra incentives and AI expenditure does the same. But doesn’t all this lead to additional upward pressure on inflation, to which consumers are extremely sensitive? The OECD, the club of established industrial countries, predicts that US inflation will increase slightly in 2026, to 3.2 percent.

The question becomes whether the central bank, the Federal Reserve, is able and willing to reduce inflation next year. That is one of its core tasks. The Fed aims for 2 percent inflation, and should keep interest rates relatively high to curb lending and reduce inflation from the current 3 percent to that 2 percent target.

Interest rate easing

Things will be very exciting around the ‘Fed’ in 2026. The chairman of the central bank, Jerome Powell, is saying goodbye. It is not yet known who will replace him. But the White House is making a lot of effort to appoint someone who is sympathetic to the Trump administration. And Trump wants the Fed’s key interest rate, now between 3.5 percent and 3.75 percent, to be lowered further. This makes borrowing cheaper and stimulates inflation.

Trump previously tried to fire permanent board member Lisa Cook due to what turned out to be an unfounded accusation of That failed. In the meantime, Stephen Miran, the architect of Trump’s Mar-a-Lago plan for the economy, has been appointed to the board.

Trump himself has already announced that interest rates need to be lowered by another full percentage point. That’s not what he’s about: the Fed is supposed to operate. But he may still have influence through the board and the chairman. In addition to Kevin Hasset, a convinced Trumpist, the incumbent Fed director Christopher Waller is also a candidate to take over from current chairman Powell. And this week, after a ‘job interview’ with Trump, this Waller repeated his preference for an interest rate cut by 1 percentage point.

The problem is that the rule of thumb that the Fed itself uses, the so-called Taylor ruleimplies that the current interest rate is actually already slightly too low given the economic situation and inflation. Many more interest rate cuts in 2026 therefore seem unwise for the time being. An even looser monetary policy risks inflation spiraling out of control because the central bank keeps interest rates too low under political pressure, which also happened in the 1970s under Fed Chairman Arthur Burns and President Nixon.

A new monetary regime

The economy is currently being fully stimulated with tax cuts, relatively low interest rates and record investments in AI. That may be good for economic growth in the short term, but at the same time inflation could become – and remain – high in the long term. It could explain the simultaneous boom in shares (.

Who is right here? Inflation makes voters angry. The affordability of daily existence – which in the US is referred to as ‘affordability’ – is high on the agenda. Democrat Zhoran Mamdami was elected mayor of New York last month because he strongly emphasized this.

An unusually defensive Trump told Americans in a televised speech last week that a fantastic era is just around the corner, with high growth in prosperity and radically falling inflation. He also spoke of drops in drug prices of 500 percent, a mathematical oddity that would mean that for a pack of paracetamol that used to cost $5, you now get $20. While he previously got away with such hyperbole, this time most reactions were negative.

None of this alters the fact that there may be a political interest in higher inflation. The American budget deficit is now above 7 percent and, according to most forecasts, will remain there for the time being. The economy is therefore growing partly on government credit, and the rising national debt also shows this. This already amounts to 123 percent of GDP and will increase towards 130 percent in the coming years. That is almost one and a half times the average debt of the euro countries.

Inflation erodes debt. The US now pays more than 4 percent of GDP in interest on its debts annually, more than on the defense budget, which puts less pressure on the budget if the money is less

But inflation also erodes the exchange rate of a currency in the long term. Should we prepare for a new American monetary regime in the near future, which will kill two birds with one stone with a higher inflation target than the traditional 2 percent: a cheaper dollar and a melting debt? That would be unwise. Because the bill will come later, in the form of inflation that takes on a life of its own and sky-high interest rates that are needed to suppress it. Just like the late seventies. But Donald Trump doesn’t seem like the person to worry about that. About history, nor about the long term.

In 2025, the stock market gained such enormous value that it begins to dominate the economy, instead of the other way around. And debts and deficits are rising so high that they influence interest rate policy. Donald in Wonderland. How does that work out? The year 2026 will be incredibly exciting.

The journalistic principles of NRC