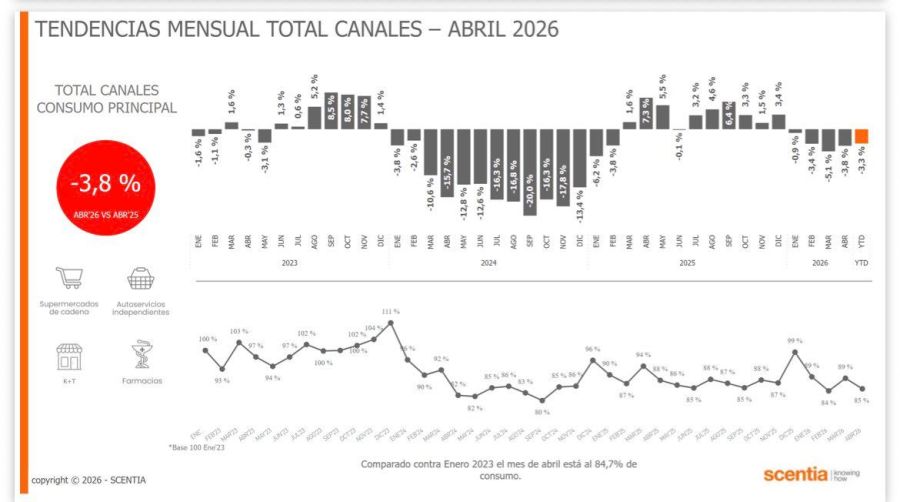

The consultantto Scentia once again raised an alarm bell about the evolution of consumption in the country by releasing its latest survey corresponding to April of this year, where it recorded a 3.8% year-on-year drop in sales of mass consumption products. The data confirmed that the inflationary slowdown observed during that month has not yet been able to translate into a recovery in household purchasing power or a sustained improvement in commercial activity linked to food, beverages, cleaning and personal hygiene. The report also marked a monthly decline of 4.7% compared to March and an accumulated contraction of 3.3% in the first four months of the year.

The work disseminated by the consulting firm directed by Osvaldo del Rio showed that the deterioration in consumption remained practically widespread in all traditional marketing channels. The large supermarket chains were once again among the most affected sectors, with a decrease of 4.5% year-on-year and an identical decrease in the monthly comparison. Independent supermarkets fell 3%, while kiosks and neighborhood stores suffered a drop of 4.8%, consolidating the deterioration of local businesses that depend on the daily spending of families. Wholesalers, historically used by consumers to reduce costs through volume purchases, also registered a drop of 4.5%, reflecting that even savings strategies began to lose dynamism.

One of the most significant data from the survey was that the only channel with significant growth was once again electronic commerce. According to Scentia, the e-commerce It showed an increase of 40.4% year-on-year and consolidated itself as the main exception within a recessive scenario. The phenomenon reveals a change in purchasing habits, where some consumers prioritize digital promotions, bank discounts and online platforms to maintain minimum levels of consumption. However, the report itself clarified that the specific weight of electronic commerce is still not enough to compensate for the structural decline of traditional physical channels.

Pharmacies appeared as another of the few segments that managed to avoid completely negative numbers, although with practically stagnant results. The report indicated a slight year-on-year improvement of 0.1%, although when comparing April against March the item showed a sharp drop of 9.4%, which showed that not even products associated with health and personal care managed to fully escape the adjustment of domestic spending.

The analysis by product categories allowed us to observe more clearly how the consumption priorities of Argentine households changed. “Impulsive” items, linked to non-essential or occasional purchases, led the declines with a 12% year-on-year drop. Perishable products (-7.8%), breakfast and snacks (-7.6%), clothing and home cleaning (-5.9%) and food (-3.6%) also fell sharply. Even hygiene and cosmetics showed a decrease, although more moderate, of 0.3%.

Within this panorama, the only categories that managed to grow were alcoholic beverages and non-alcoholic beverages, with advances of 6.7% and 4%, respectively. Sector analysts interpreted that this behavior can be linked both to aggressive promotional strategies of brands and to seasonal changes in consumption. The greater presence of these categories within digital platforms and discount chains also influences.

The Scentia report also put the spotlight back on a phenomenon that has been affecting the Argentine economy for more than two years: the loss of disposable income of families. Although inflation began to slow down in April and stood at 2.6%, compared to 3.4% in March, salaries still show difficulties in recovering from the accumulated increase in prices of rates, transportation, education and services. According to different private consulting firms cited by economic media, a good part of household income continues to be concentrated in fixed expenses, reducing the purchasing capacity of daily consumption goods.

The deterioration of mass consumption was also exposed when compared to previous months. In March, the same consulting firm had recorded a year-on-year drop of 5.1%, while February had also shown negative numbers, consolidating a trend that has already accumulated several consecutive months in the red. In that report, supermarkets and wholesalers had suffered even more pronounced declines, of 7% and 8.8%, respectively, which showed that April showed a slowdown in the magnitude of the fall, although still far from any concrete recovery.

From Scentia they maintained that consumption behavior could begin to stabilize if the inflationary slowdown consolidates in the coming months. The consulting firm pointed out that the “weighted average price of mass consumption” maintains a downward trend and that a sustained improvement in macroeconomic variables could generate a positive impact on sales towards the second semester. However, businessmen in the sector warned that they still do not see firm signs of recovery and described the current scenario as one of extreme caution among consumers.

The picture left by April thus showed an economy where the slowdown in inflation is still not enough to modify the defensive behavior of households. The fall in mass consumption became one of the main thermometers of the social and economic situation, reflecting that a large part of the population continues to prioritize essential expenses, postponing purchases and reducing the volume of consumption even in basic products.

Image gallery

![]()