In 2024 there was an impressive reversion of fiscal dynamics. Of a financial imbalance equivalent to 4.6% of GDP in 2023, a 0.3% financial surplus of GDP was passed in 2024. An increase in the financial surplus of almost 5% of GDP was achieved. The adjustment is explained by a drop in all components of primary spending (that is, excluded disasters interest). While public income remained constant in 16.8% of GDP, all components of primary expenditure were dropped in real terms that totaled a total reduction of 4.5% of GDP. To achieve this, the expense liquefaction in a high inflation environment was key.

The challenge is now to sustain the surplus in a context of low inflation. In some expenses, it reaches to follow the same strategy, such as sustaining the decrease in the salary mass with the reduction of public employees and an austere salary policy. In the case of retirement, without prejudice to the fact that an integral order is very important, with the mobility that establishes increases based on inflation, short -term dishes will be controlled, if the moratoriums that expire in March are not renewed.

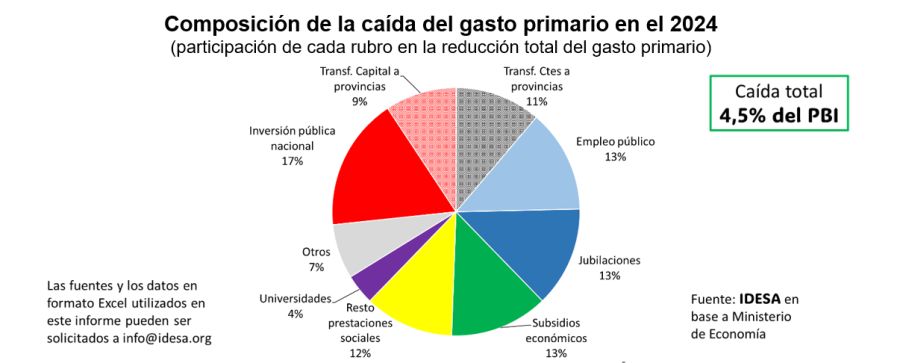

But there are other expenses where an urgent change of strategy is needed. These are the cases of discretionary transfers to provinces and investment in infrastructure. According to the Ministry of Economy between the 2023 and the 2024 It is observed that:

– The fall in national transfers for current expenses of provinces represented the 11% of the total fall of primary expenditure.

– The fall in national capital transfers to provinces explains another 9%.

– The fall in national investment in interprovincial functions represented another 17% of the primary expenditure adjustment.

These data show that More than a third of the reduction of primary expenditure was thanks to the reduction of non -automatic transfers to provinces (currents and capital) and investment directly executed by the nation. In the case of national investment, government announcements are in the direction of seeking mechanisms for private companies to take over the maintenance and development of new infrastructure. It is a process as complex as it is urgent. But even more challenging are the problems that derive from the drastic reduction of non -automatic transfers to the provinces.

The reduction of transfers to the provinces is in the right sense of eliminating overlaps that are sources of inefficiencies. However, Because it has been done unilaterally there is a risk that the provinces and municipalities reacting increasing taxes. It should be taken into account that two of the worst taxes – gross and industry and trade rates – are the main sources of financing of the provinces and municipalities. Thus, a powerful erosion factor of competitiveness for national production is formed that is the combination of exchange rate appreciation with rises of gross income and municipal rates and the deepening of the deterioration of the infrastructure, because the three levels of government reduced the public investment.

To preserve the fiscal surplus and contemplate the problems of competitiveness, a tax coordination agreement between the Nation and the provinces is essential. A first component of the agreement should be the Functional ordering of the public sector. This is to clearly specified the functions of each level of government: the National State executes interprovincial functions and the provinces with their municipalities take over local functions. The objective is to eliminate the overlapping that damage the quality of public management. The other component must be the Tax planning. Also eliminate tax overlaps and clearly establish which tribute finances to each level of government. In this way, co -participation is replaced by the fiscal correspondence in which each level of government addresses its function with the resources it produces.

The strong fiscal adjustment allowed to overcome the critical situation that had been reached at the end of 2023. But It is very important to prevent the almost elimination of transfers to the provinces from increasing taxes aggravating competitiveness problems. Therefore, it is important and urgent to sign a tax coordination agreement.

*Jorge Colina is an economist and president of IDESA

By Jorge Colina

Image gallery

![]()