There’s something surreal about it. More this Saturday morning the (for now) last tanker with kerosene from the Strait of Hormuz in the port of Rotterdam. This week, responsible European Commissioner Dan Jørgensen warns that the energy crisis will last longer and that he is preparing tough measures to reduce energy consumption. And on top of that, the US is sending thousands of troops to the Gulf region and Iran continues to hit oil and gas facilities in neighboring countries every day. And in the midst of all that, stock markets worldwide experienced something of a ‘recovery week’.

Since the start of the American-Israeli war against Iran on February 28, many Western stock indices had hesitantly slid down into ‘correction territory’ (at a minus of 10 percent compared to the highest price, stock market analysts speak of a correction). But on the waves of President Donald Trump’s once again baseless claims last Thursday that the war would be over sooninvestors regained their optimism. The stock markets in Asia opened sharply on Friday, while in Europe and the US there was no trading on Good Friday.

The market is always right, according to stock market wisdom. The main question here is: which market? Equity investors have reacted excessively sharply to news from the Gulf region in recent weeks. Every announced deterioration of the situation led to sharp falls in prices, while optimistic messages on social media and in interviews by Trump could push prices back up by percentages in just a few hours. The same applied to the price of oil, which could rise or fall by many dollars in a matter of hours, depending on what news came out of the White House.

Ostriches and hysteria

Stock markets have not been a reliable indicator of the underlying economic reality for some time now. Analysts make the comparison with the beginning of the corona pandemic, where investors also seemed deaf to the major economic consequences of the virus for a long time. Only when the impact could no longer be denied did prices collapse. Once again, a combination of ostrich politics and hysteria seems to play a greater role than careful economic analysis of the dire situation in which the world finds itself.

Energy inflation is particularly worrying: it went from -3.1 percent to 4.9 percent

That situation became clearly visible this week in the inflation figures for March. European statistics agency Eurostat reported annual inflation of 2.5 percent for the eurozone, an increase of 0.6 percentage points compared to February. The increase in energy inflation was particularly worrying: it went from minus 3.1 to plus 4.9 percent. This is normally a precursor to so-called second-order effects: since everything and everyone needs energy to run the economy (transport, heating, light, machines), it is a matter of time before those high energy prices become anchored in the rest of the production chains and in wages.

The sharply rising inflation (also in Asia and the US) is putting pressure on central banks. Their task is to halt monetary depreciation by raising interest rates. Analysts now take into account that the European Central Bank (ECB) will raise interest rates three times by a quarter of a percentage point this year in response to the consequences of the energy crisis. This is necessary to curb inflation, but painful for the already faltering economic growth: higher interest rates put a brake on investments and therefore on growth. A period of stagflation (stagnant growth in combination with high inflation) is looming.

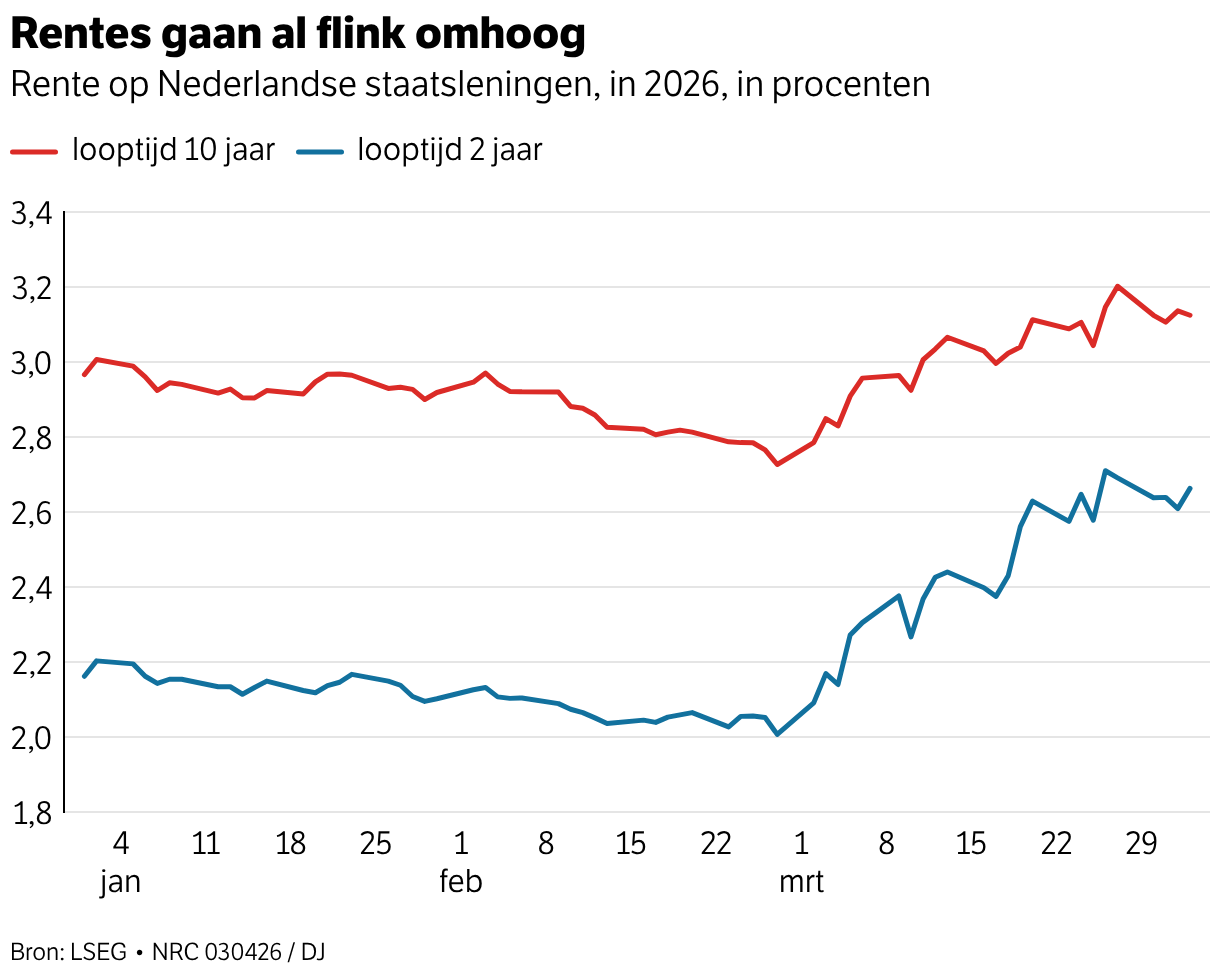

This scenario of higher interest rates and slower growth may be ignored by the stock markets, but the malaise is already clearly visible and palpable in other markets: market interest rates on both corporate and government bonds have risen sharply since the start of the war. For example, the interest rate on a short-term, two-year US government bond was 3.37 percent a month ago, but at the beginning of this week it peaked at 3.98 percent. The ten-year government bond went from 3.9 to more than 4.4 percent in a few weeks. The interest rate on Europe’s leading German government bond with a ten-year term has now risen above 3 percent (from 2.4). Following the rising interest rates on government debts, mortgage interest rates are also creeping up: on a Dutch mortgage with a term of ten years, the interest rate is now 4 percent, before the war it was 3.7 percent.

And government bonds are still relatively popular because corporate bonds are becoming too risky. This means that interest rates on those business loans also rise, making borrowing considerably more expensive for companies. The disaster is also already palpable in the private credit market. If growth slows down, companies’ growth scenarios evaporate. The risk of investments is therefore increasing, and many investors are already withdrawing their money from private lenders and high-risk corporate bonds.

Private credit provider Blue Owl, which provides loans directly to tech companies and private equity firms without the intervention of a bank and now manages $300 billion, had to report this week that $5.4 billion in investments had been withdrawn. Investors actually wanted to take away a lot more moneyafter which the company was forced to announce a recording stop. Other investment vehicles such as KKR, Ares Management, Apollo Global and BlackRock’s HPS Investment Partners have also taken similar measures to prevent an emptying of their investment funds. In the first quarter, investors attempted to withdraw approximately $19 billion from these credit funds, said the Financial Times.

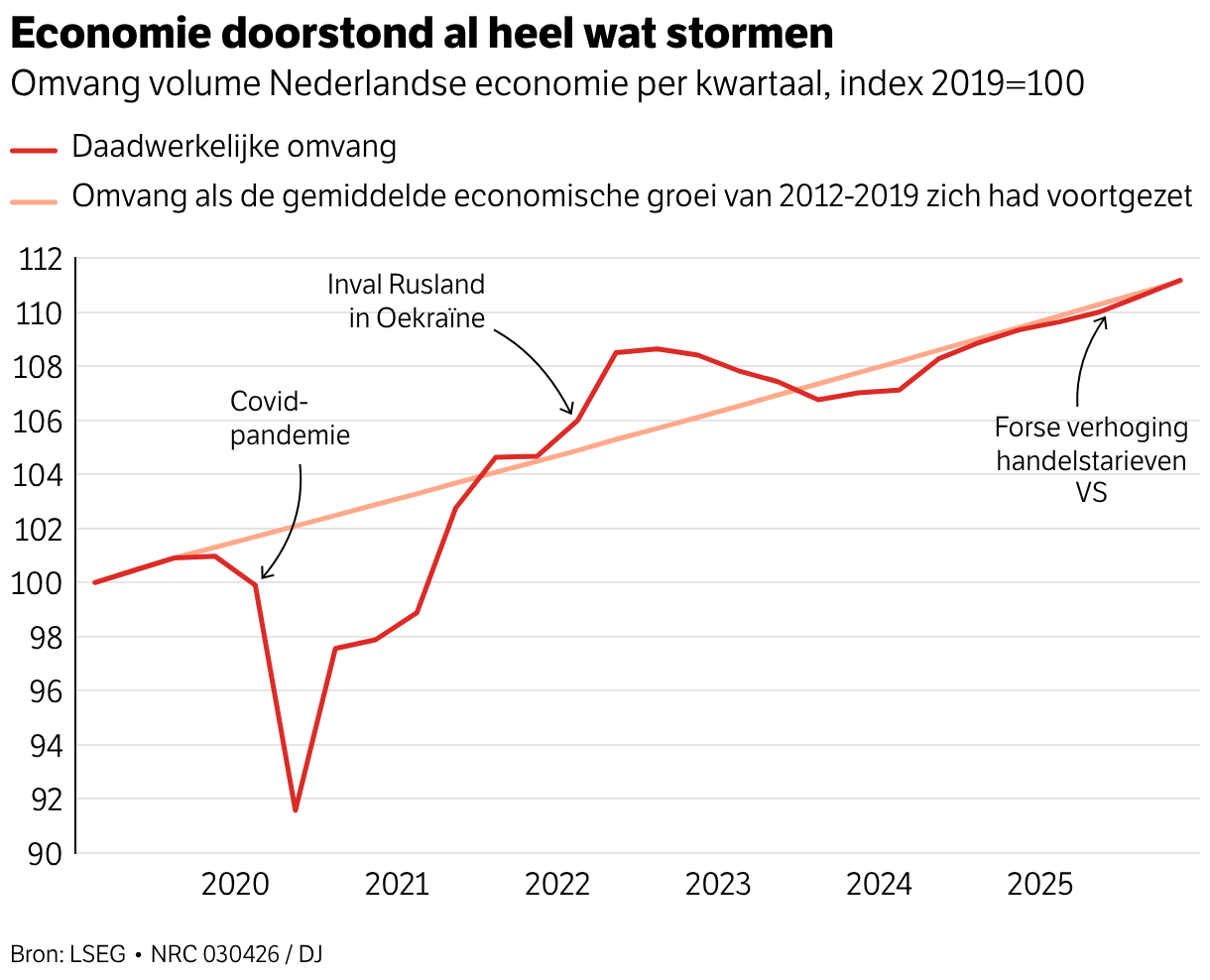

It is striking how well the Dutch economy has weathered the recent crises

With open mouth

All disasters, led by the energy crisis, are causing economists from major banks and institutions to significantly reduce their forecasts. Predictions for inflation approaching 4 percent are no longer unusual. This also applies to economic growth that falls well below 1 percent.

And that raises the question: can the economy withstand another major shock? Olaf Sleijpen, the president of De Nederlandsche Bank, emphasized last month during the presentation of the central bank’s annual report that crises are a kind of business as usual are becoming: “This annual report is published, I might say traditionally, at a time when we are all watching with open mouths what is now happening on the world stage,” he said.

All recent shocks have been accompanied by warnings from economists that very severe weather was on the way. This was the case with the Covid pandemic (February 2020), with the Russian invasion of Ukraine (February 2022) and the extreme increase in US import duties for friend and enemy by US President Trump (April last year).

All these events were certainly not without consequences. But what is striking is that the Dutch economy withstood them quite well. The damage from Covid – a deep decline in gross domestic product – was reversed in the fourth quarter of 2021 after an equally strong recovery. The same happened after the energy shock caused by the invasion of Ukraine. And the consequences of Trump’s tariff offensive worldwide were not as bad as had been feared – although this is mainly due to the fact that America’s trading partners did not or only partially hit back with their own tariff increases – with the exception of China. A real trade war was thus prevented.

The surprising outcome: if the shocks had not occurred and the average economic growth from the pre-Covid period – just under 0.4 percent from quarter to quarter – had continued to occur, the Dutch economy would now be as large as in the real world with all the shocks.

The only major change since the prelude to Covid is a significant and lasting increase in the Dutch price level, and with some delay also the level of wages. Because inflation was very high and persistent, and employees wanted a growing income in return so as not to lose purchasing power. If inflation of 2 percent had occurred since the start of Covid – the target of the European Central Bank, the price level in the Netherlands would now be 13 percent higher than then. In reality it is now almost 30 percent higher.

One punch away from knockout

Two different conclusions can be drawn from the entire course of events: even now, during and after the Iran crisis, doom predictions will later prove to be rather exaggerated. The economy has proven to be more stubborn than expected, and will continue to be so.

But another conclusion is also possible. Are the reserves now gone, after taking so many hits in a row? Like a boxer who is still standing after three rounds, but is now only one punch away from a knockout.

Although forecasts among economists differ slightly, there is great agreement on one thing: the severity of the economic consequences depends mainly on the duration of the Iran crisis and its consequences. The scenario of a short and fierce conflict around Iran has long been in the trash. European Commissioner Dan Jørgensen’s warning that the energy crisis resulting from the war will last a long time only reflects a growing consensus in this respect. But the damage is not the same for everyone.

Developing and emerging countries, especially in Asia, are already experiencing energy shortages, sharply rising costs and social suffering. Europe and the Netherlands, which can better afford expensive energy prices on the world market, can keep the damage relatively limited in comparison – although Jørgensen warns that energy rationing will not be unthinkable here either.

Essentially, it is the United States itself, now the largest oil producer and exporter of liquefied gas, that is seeing the least direct impact of the crisis – although rising petrol prices are being made a big deal for political reasons. Call it irony: the economy of the country that helped start the Iran war has so far suffered the least. Perhaps it is precisely this cynical observation that is supporting prices on Wall Street for the time being.