2023 ended with inflation greater than 200% annually. This was a product of the chronic and growing accumulation of fiscal deficits. The national Treasury debt reached the equivalent of 67% of GDP. At this point the possibilities of financing deficits with increases in Treasury debt were exhausted.. The proof was the dizzying increase in country risk (the additional interest rate that the Argentine national State must pay for its debt with respect to the United States) which exceeded 2,000 points. This involved paying a 20% annual interest rate above the income paid by bonds issued by the United States.

Given the impossibility of continuing to issue Treasury debt, fiscal deficits were covered with monetary issuance. As excess issuance generates pressure on inflation, the Central Bank appealed to remove part of that money from circulation by issuing settlement letters (leliq).. Commercial banks used their clients’ deposits to give them to the Central Bank in exchange for leliq. In this way, chronic fiscal imbalances led, in addition to generating high inflation, to accumulate debt from the Treasury and the Central Bank (Leliq).

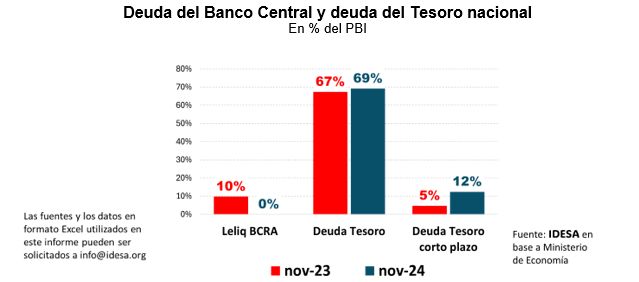

What happened to the Leliq in the current government? According to the Central Bank and the Ministry of Economy, between November 2023 and November 2024 It is observed that:

– The leliq went from 10% from GDP to 0%.

– The national Treasury debt increased 67% to 69% of GDP.

– The Treasury’s short-term debt increased 5% to 12% of GDP.

These data show that the disappearance of the leliq was achieved by replacing them with Treasury debt. At a consolidated level, the debt remained at similar levels, but a more transparent and consistent accounting record was adopted. All the debt of the national public sector was registered in charge of the person who generated it (the Treasury) and the Central Bank was freed from managing the leliq to finance the fiscal deficit. This honesty occurred without going through traumatic episodes such as a “Bonex plan” (that is, compulsively exchanging the leliq for a long-term security that is delivered to bank depositors) or hyperinflation (that is, liquefying the value of the leliq and the deposits that backed them).

The main lesson that this experience leaves is that the central problem was not the magnitude of the debt but the magnitude and persistence of the fiscal imbalances that fuel the debt.. If the flow is cut off (fiscal balance) the stock (debt) is manageable. The clearest evidence is the dizzying drop in country risk. To the extent that this trend continues – for which it is key to provide certainty about the sustainability of the fiscal balance – it will be feasible to renew debt maturities with market operations without the risk of facing traumatic situations that force us to appeal again to the Central Bank. .

It was demonstrated that fiscal balance is a very powerful instrument. The critical debt situation that had been reached at the end of 2023 seemed like it could only be overcome by facing hyperinflation that liquefies the leliq or the exchange of the leliq for a long-term bond. However, the government opted for a strong adjustment in public spending, migrating from chronic and high financial deficits to surpluses. This reversal in the result of public finances allowed, without confiscation, to eliminate the leliq. Thus it became evident that the enormous importance of ending the chronic imbalances of the State had been underestimated.

To continue these achievements, it is essential that the fiscal balance be sustainable. This will only be possible by moving from the adjustment of the State to the comprehensive ordering of the State.. The founding point of this transformation is a fiscal coordination agreement between the Nation and the provinces that specifies the functions that each level of government has the exclusive responsibility of addressing (so that the national State stops overlapping expenses with the provinces and municipalities). and the taxes with which each level of government will be financed to meet the exclusive responsibilities it has to attend to.

*Jorge Colina is an economist and president of IDESA.

by Jorge Colina

Image gallery

![]()