Only 4 percent of all stocks ever listed account for the entire increase in wealth in the US stock market since 1926. The rest? Underperforms government bonds in the long term. The question is not whether you should buy stocks – but rather how you find the few long-running stocks and avoid the rest. Billionaires like Warren Buffett don’t use gut feeling, but rather a system. Here’s ours: five points that even beginners can use right away.

The truth is harsh: Long-term studies (e.g. by Hendrik Bessembinder) show that only a very small proportion of all stocks ever listed – around 4% – explains the total net asset growth of the US stock market since 1926. The vast majority of individual securities perform worse than government bonds in the long term. Only a few “super stocks” pull the average up. But how do you find these rare endurance runners that you can keep “forever”?

The answer lies not in chart technology or daily news, but in one systematic, cool look at the company itself. Billionaires like Warren Buffett don’t operate Tradingthey operate Business analysis. It’s exactly this approach that we’re distilling down today clear 5-point gridwhich even beginners can use immediately to avoid the emotional traps of the market and systematically search for the best stocks for long-term wealth creation.

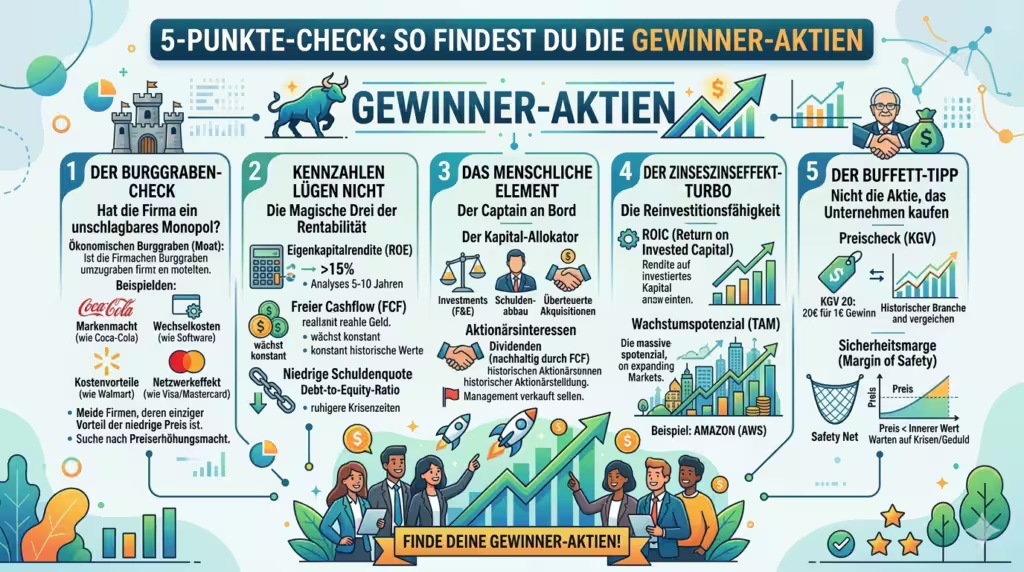

1. The moat check: does the company have an unbeatable monopoly?

The biggest problem most companies face? They are interchangeable. Low entry barriers, tough price wars – this eats up margins and makes shareholders poor. Your first check must therefore always be the question of whether the business model is compatible “economic moat” owns.

- What is the Moat? It is a sustainable competitive advantage that protects the company from the competition.

- Examples of moats: Intangible assets (brand power like Coca-Cola, patents), Switching costs (Software providers whose products are deeply anchored in customer processes), Cost advantages (Walmart, which can buy and sell more cheaply than its competitors thanks to its enormous purchasing power and logistics efficiency) or the Network effect (Platforms like Visa or Mastercard, which become more valuable the more people use them).

Your focus: Avoid companies whose only advantage is their current low price. Search for companies that prices can increasewithout losing customers. This is the ultimate evidence of a moat.

2. Key figures don’t lie: the “magic three” of profitability

The biggest illusion in the stock market is the belief that high Sales automatically lead to prosperity. Error! Many fast-growing companies just burn capital. What matters is that profitability. Focus on these three simple metrics over a minimum period of time five to ten years:

- Return on equity (ROE – Return on Equity): How efficiently does management use the owners’ money? A consistently high ROE of over 15% is a fantastic signal. It shows that the company can generate new, profitable growth with the reinvested profits.

- Free Cash Flow (FCF): This is the “real” money that is left over after all necessary investments and is freely available for dividends, share buybacks or debt reduction. The FCF should grow constantly and is often the case with particularly profitable business models at or above the level of net profit – a quality signal that shows that the profits actually arrive in the company as money. In capital-intensive sectors such as industry, utilities or telecommunications, the FCF is often structurally below the net profit, without this necessarily being a warning signal – an industry comparison is worthwhile here.

- Low debt ratio: Companies with little debt (lower Debt-to-equity ratio) sleep more peacefully in a crisis. They are less dependent on banks and can use their profits for growth instead of paying interest.

The trap: A uniquely good value is coincidence. Only those historical consistency These key figures demonstrate the quality of the business model.

3. The human element: count on management

Even the best business model can be ruined by incompetent or self-serving management. The “captain” on board decides long-term success. But how do you judge that?

- The capital allocator: Don’t look at the CEO’s vision, but rather, how he spends the money. Is he investing wisely in future projects (R&D), reducing debt, or buying overpriced companies just to expand his own empire? A look at the history of Acquisitions is often more insightful than any glossy presentation.

- Shareholder friendliness: Have shareholders been treated fairly in the past? They rise Dividends not only, but they are also sustainably covered by the FCF? (Keyword: dividend aristocrats). Danger: Is management constantly selling its own shares while spreading good news? That is a Red Flag.

4. The compound interest effect turbo: the ability to reinvest

The most important engine for decades of wealth creation is the compound interest effect. With stocks this means: the company has to restore its profits extremely profitable can create.

- High return on invested capital (ROIC): This key figure shows how much profit a company generates for every euro invested. Companies like Apple and Microsoft shine here.

- The growth potential: Does the company have one? gigantic target market (Total Addressable Market, TAM)which can still grow in ten or twenty years? Anyone operating in a shrinking market will eventually reach their limits, no matter how good the management is.

- Example Amazon: They used the cash flow from bookselling to reinvest in cloud computing (AWS) – a decision with absurdly high ROICwhich made them one of the most valuable companies in the world.

5. The Buffett tip: don’t buy the stock, buy the company

Even the best company in the world is a bad investment if you turn it into one absurdly high price buy. This is the part of the analysis that discipline requires.

- The price-earnings ratio (P/E ratio) as a price check: The P/E ratio indicates how many times the annual profit you pay for a share. A P/E ratio of 20 means: You pay 20 euros for every 1 euro of profit. Don’t just compare the current P/E ratio with that Industry averagebut above all with that historical P/E ratio for the last ten years of the company itself.

- The margin of safety: Only buy the stock if its price is significantly below your estimated intrinsic value. Warren Buffett would never buy a great suit at full price – why would you do that with a stock? Patience is the most important factor here. Wait for the price to dropcaused by a crisis or temporary bad news, and then strike.

Conclusion: start your own system – and eliminate fear

Finding the “right” stocks is not a guessing game; solid business model analysis. Most investors fail not because of a lack of intelligence, but because of a lack of intelligence structure and emotional discipline.

Your Actionable tip: Take a blank sheet of paper or an Excel spreadsheet and create this for each stock that interests you 5 point grid. Award one point for each criterion met. Only stocks that at least four out of five points achieve, end up on your watchlist at all.

Please note: Not all five criteria are equally important. A missing moat or a valuation that is significantly too high should generally not be compensated for by other strengths – these two points are the foundation on which the others are built.

You now have the blueprint of the most successful long-term investors. Control of your financial future is in your hands – but only if you learn like a business owner and not like a gambler to think. The first step has been taken. Start today, not tomorrowwith your own incorruptible rating system.