Hardly any other topic is currently electrifying the stock market as much as artificial intelligence. Anyone who got into Nvidia, AMD or Palantir early may see dream profits in their portfolio – and anyone watching will feel the growing pressure to finally “get a piece of the cake”. But the euphoria also has a downside. Valuations are rising to dizzying heights and several voices are warning of an AI bubble. Many investors are asking themselves the same question: Is this the beginning of a revolution – or perhaps the beginning of the end?

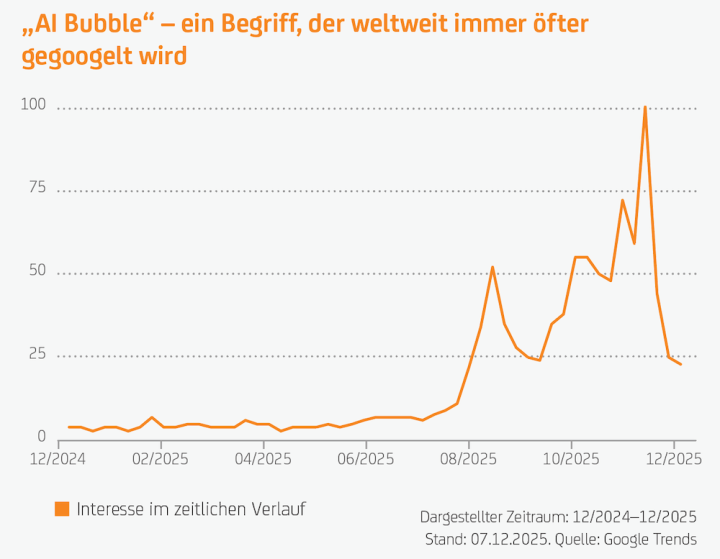

![]() In recent months, the term “AI bubble” has become a staple of financial reporting. Whether in business media, comments or social media – hardly a day went by without warnings about a possible “AI bubble”. Proof of this is the frequency of searches for this term, as shown by Google Trends data. The topic has achieved a media presence that is almost becoming an argument against an imminent bubble. Real speculative bubbles usually burst when hardly anyone is aware of their existence.

In recent months, the term “AI bubble” has become a staple of financial reporting. Whether in business media, comments or social media – hardly a day went by without warnings about a possible “AI bubble”. Proof of this is the frequency of searches for this term, as shown by Google Trends data. The topic has achieved a media presence that is almost becoming an argument against an imminent bubble. Real speculative bubbles usually burst when hardly anyone is aware of their existence.

This high level of attention probably reflects the general uncertainty and nervousness of many investors rather than a concrete warning signal that the bubble is imminently bursting. In order to better understand the situation, the Investment Institute by UniCredit took a look at the latest developments.

Billions in investments are fueling bubble fears

The scale of capital investment in AI is impressive. Big Tech is investing billions of dollars in the technological foundation, including data centers, high-performance chips and power generation, but also concrete, steel and power lines. Net capital spending by major U.S. companies has already exceeded dot-com bubble levels. The investments are made in advance, but what the returns will be remains to be seen. Hardware cycles add pressure: GPUs typically lose value within three to four years. Even if their lifespan extends somewhat, it remains limited compared to the decades-long lifespan of dot-com-era fiber optic infrastructure. Despite the speculative nature of the time, the investments made at the time ultimately created enduring physical structures that still support the global Internet today.

The current expansion is supported by the robust cash flows of the tech giants, whose financial strength makes them strong drivers of the AI cycle. But as investment needs continue, hyperscalers are increasingly looking for ways to reduce direct capital intensity, for example by outsourcing computing capacity to smaller neocloud providers. However, they do not have comparable financial strength and are often heavily dependent on equity and debt capital to expand their capacities. The use of debt capital is likely to play a larger role in the entire AI ecosystem in the future – not just among smaller players. Meta’s latest $30 billion bond offering marks the first major move by Big Tech to finance AI infrastructure through debt, a new dynamic that increases systemic risk.

These developments and the continued rise of leading technology companies in the AI space have led to investors becoming concerned about whether the AI story is overpriced. There are elements in investment behavior and market prices that rhyme with previous bubbles, including the rise in absolute valuations, high market concentration, increased capital intensity of leading companies, and the emergence of seller financing (where suppliers provide financing or credit to their customers to force purchases of their own products).

Bubble? No. Correction? Perhaps.

However, the Investment Institute believes the technological environment continues to favor AI investments for two reasons:

- First, AI applications increase productivity when deployed.

- Second, unlocking these productivity benefits requires significant computing power, especially since models grow much faster than the necessary computational steps and energy costs fall.

To assess whether fears of a bubble are justified, one must consider the current fundamental situation. So far, the relevant tech companies have been driven more by strong and sustainable profit growth than by irrational speculation about future growth.

The strong earnings momentum was a key driver for the recent price increases. While this is reassuring as it reflects solid fundamentals, it also suggests that the current rally is heavily dependent on continued earnings performance. Most stocks are currently trading at high valuations compared to their historical averages. However, the rise in valuations is largely underpinned by strong underlying profitability and a robust return on equity. These developments do not indicate a speculative bubble in technology or AI. Rather, they reflect broader macroeconomic conditions: the shift toward monetary easing after a period of elevated interest rates, significant global savings and a sustained business cycle. All of these factors have contributed to a favorable environment for risk asset valuations. While high valuations make markets vulnerable to a correction if confidence in economic growth weakens, such a downturn is unlikely to be triggered by a slump in the technology sector alone.

Actively invest selectively in AI

Even though the discussion about a possible AI bubble could hardly be louder at the moment, there is much to suggest that artificial intelligence and related technologies will play a central role in our lives and in the markets in the long term. At the same time, the selection of companies is becoming increasingly important. Not every company that is in the spotlight today will still be a winner in ten years. Investors who believe in the future of AI but do not want to blindly follow the hype can therefore rely on actively managed fund strategies that attempt to identify innovations at an early stage and at the same time diversify more broadly.

An example of this is the onemarkets Rockefeller Global Innovation Equity Fund. The fund invests worldwide in companies whose products, services or business models not only correspond to current trends, but also have the potential to shape entire industries in the future. To achieve this, portfolio management combines the decades of experience of the Rockefeller research team with its own screening process. This specifically identifies companies with a clear innovation orientation – for example in the areas of technology, health, demographics or decarbonization. The result is a concentrated portfolio of 50 to 70 stocks.

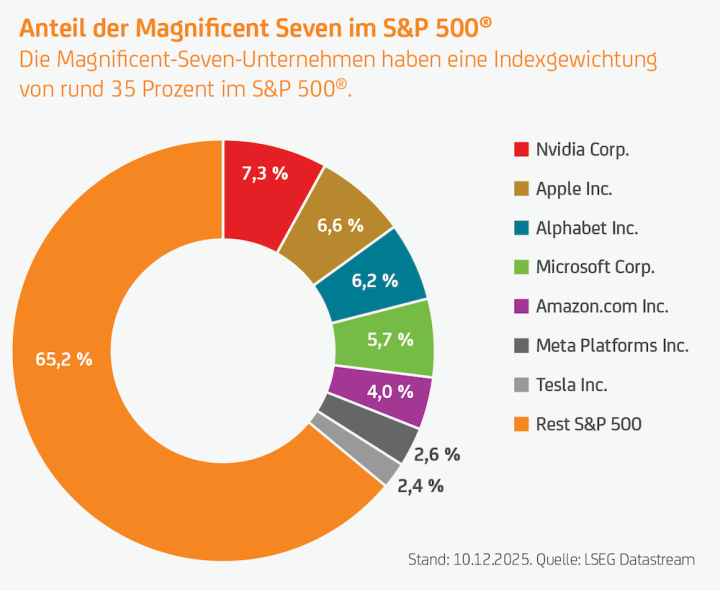

Currently, around 40 percent of the portfolio weighting is in the IT and telecommunications sector. These include well-known companies such as Microsoft, Alphabet and Meta, all of which are key players in the field of artificial intelligence. Thanks to their profitable business models and high cash flows, they can invest enormous amounts in research, development and the expansion of data centers. These opportunities are not available to many smaller companies and start-ups to the same extent. The portfolio is supplemented by, among others, Nvidia and TSMC, two “shovel manufacturers”. The term comes from the gold rush and describes companies that do not search for “gold” themselves, but provide the equipment – in this case the chips and semiconductors that form the technological basis of the AI boom. However, if the momentum in the AI sector weakens and the market experiences a correction, these strongly AI-driven companies could react particularly sensitively.

Weight sectors flexibly

Another component that can help investors remain flexible in the dynamic technology sector is the new onemarkets UC US Sector Rotation Strategy Fund. The fund takes a rules-based approach that systematically leverages the strengths of various U.S. sectors. Instead of selecting individual companies, the portfolio management with this strategy invests in entire sector baskets and regularly adjusts their weighting to the market environment.

The basis for this is the UC US Sector Rotation Net Return Index developed by UniCredit. This index uses the long-term real return published by the U.S. Treasury as a signal of the economic cycle. Depending on the signal, the index switches between two fixed sector baskets. When real returns fall, the focus is on cyclical sectors such as materials, financials, energy and consumer discretionary. As real returns rise, people move into sectors such as information technology, utilities, healthcare and communications. The allocation is checked monthly and adjusted based on rules.

Especially in an environment in which technological trends such as AI are fascinating in the long term but can also change significantly in the short term, such a rule-based approach offers more orientation. It helps to adapt the portfolio orientation to changing market conditions.

Investors should be aware that with actively managed funds they have no control over the selection of investments, meaning they are dependent on the expertise and decisions of the portfolio management. Like other investment products, equity funds are subject to market movements and may experience fluctuations that could result in capital loss.

| onemarkets Rockefeller Global Innovation Equity Fund – Fund details | ||

|---|---|---|

| Fund type | Stock funds | Stock funds |

| Investment Manager | Rockefeller & Co. LLC | |

| Fund currency | EUR | USD |

| Share class* | M | M-USD |

| Use of income | accumulating** | accumulating** |

| ISIN / WKN | LU2673954207 / A3EUHY | LU2673954462 / A3EUH0 |

| Entry costs | up to 5.00% | up to 5.00% |

| Total expense ratio | 2.20% pa | 2.20% pa |

| Minimum investment | EUR 100,– | USD 100,– |

| Savings plan | possible from EUR 25.– | possible from USD 25.– |

| * Other share classes available. ** Income from the fund such as dividends or interest is reinvested in the fund. Further information about the product can be found at: » onemarkets Rockefeller Global Innovation Equity Fund As of: December 12, 2025. Source: onemarkets (UniCredit Bank GmbH) | ||

| onemarkets UC US Sector Rotation Strategy Fund – Fund details | ||

|---|---|---|

| Fund type | Stock funds | Stock funds |

| Investment Manager | UniCredit International Bank (Luxembourg) | |

| Fund currency | EUR | USD |

| Share class* | M | M-USD |

| Use of income | accumulating** | accumulating** |

| ISIN / WKN | LU3046612167 / A4168F | LU3046612324 / A4168H |

| Entry costs | up to 5.00% | up to 5.00% |

| Total expense ratio | 2.22% pa | 2.22% pa |

| Minimum investment | EUR 100,– | USD 100,– |

| Savings plan | possible from EUR 25.– | possible from USD 25.– |

| * Other share classes available. ** Income from the fund such as dividends or interest is reinvested in the fund. Further information about the product can be found at: » onemarkets UC US Sector Rotation Strategy Fund As of: December 12, 2025. Source: onemarkets (UniCredit Bank GmbH) | ||

A notice:

UniCredit Bank GmbH (HypoVereinsbank) offers investments that can also be aimed at customers with sustainability preferences. Corresponding fund solutions are determined on the basis of exclusion criteria that are based on the concept of the German financial industry associations (common concept of DK, BVI and BSW) and are publicly available Transparency Statement | HypoVereinsbank (HVB) are visible. UniCredit Bank GmbH regularly checks the funds offered to customers with sustainability preferences once a quarter to ensure compliance with the specified criteria. The review is based on data from specialized data providers – currently ISS ESG. If the specified criteria are violated, the corresponding fund solution will no longer be offered to customers with sustainability preferences.

Photo credit:

- iStockphoto.com: Maxim Fesenko