P/E, P/S, ROE, dividend yield, operating margin – you know the abbreviations, but you don’t know which ones really count. You’re not alone. Most private investors drown in metrics and end up making gut decisions. Six values and 15 minutes are enough to separate the wheat from the chaff. Here is the quick test that professionals use.

Flood of numbers? This is how you separate the important things from the noise

The biggest hurdle isn’t the math, it’s the choice. Not every metric tells you the truth about quality. Focus on three questions: How profitable is the business? How stable and financeable are the profits? Is the price of the stock reasonable in relation to this?

This allows you to automatically sort key figures: quality, stability, rating. Everything else is an accessory. You also need context: industry, business model, cyclicality. A software provider is valued differently than a utility. So never make wild comparisons between sectors – compare within the industry.

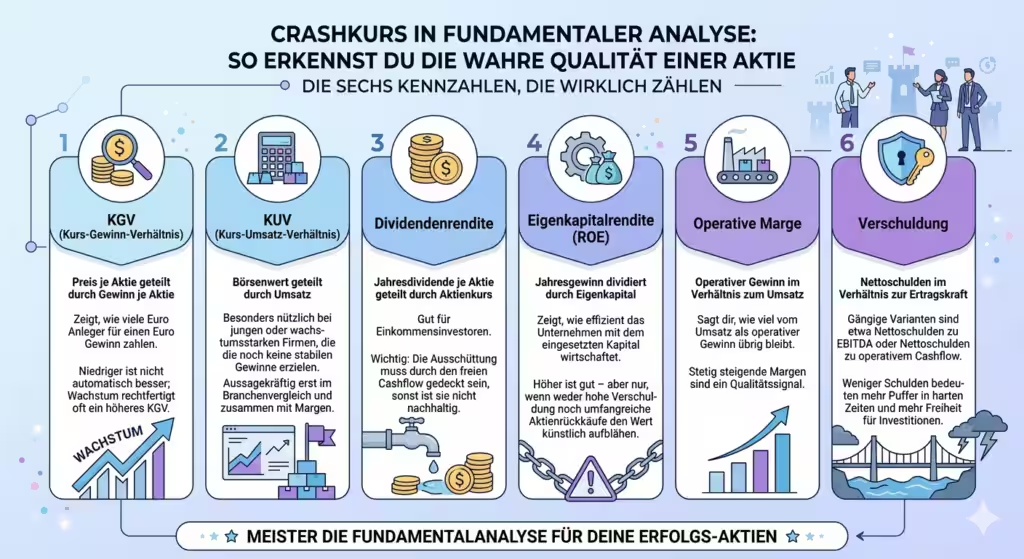

The six metrics that really count

- P/E ratio (price-earnings ratio): Price per share divided by earnings per share. Shows how many euros investors pay for one euro of profit. Lower is not automatically better; Growth often justifies a higher P/E ratio.

- KUV (price-to-sales ratio): Market value divided by sales. Particularly useful for young or high-growth companies that are not yet generating stable profits. Only meaningful when comparing the industry and together with margins.

- Dividend yield: Annual dividend per share divided by share price. Good for income investors. Important: The distribution must be covered by free cash flow, otherwise it is not sustainable.

- Return on equity (ROE): Annual profit divided by equity. Shows how efficiently the company operates with the capital it uses. Higher is good – but only if neither high debt nor extensive share buybacks artificially inflate the value. Companies with very low equity have an apparently high ROE without any actual improvement in operating performance.

- Operating margin: Operating profit in relation to sales. Tells you how much of sales remains as operating profit. Steadily increasing margins are a signal of quality.

- Debt: Net debt in relation to earnings power. Common variants include net debt to EBITDA or net debt to operating cash flow – both provide a similar picture, but are preferred differently depending on the industry and source. Less debt means more buffer in tough times and more freedom to invest.

Fifteen minutes for the initial assessment

Use this checklist as a quick test. It doesn’t replace deep analysis, but it filters reliably.

- Understand: What does the company sell and how does it make money? Recurring revenue and pricing power are pluses.

- Check stability: Sales and profit development over five years. Are they growing steadily or do they fluctuate a lot?

- Measuring quality: Operating margin and ROE. Are they stable or trending upward?

- Securing finances: Net debt in reasonable proportion to profitability. Interest payments should be easily met from ongoing business.

- Classify rating: P/E/P/S in an industry comparison. Higher growth can justify higher multiples – but not limitlessly.

- Safety margin: Plan a buffer. When assumptions easily disappoint, are you still comfortable with the price?

If you are still convinced after this quick test, it is worth doing more in-depth research: business reports, investor presentations, competitor comparisons.

Example calculations: this is how you check quality

P/E ratio: Price per share 50 euros, profit per share five euros. P/E ratio = 50 / 5 = 10. Interpretation: You pay ten times the profit. Compared to the industry: is ten low, normal or high?

KUV: Market value 1,000 million euros, sales 200 million euros. KUV = 1,000 / 200 = 5. Statement: For every euro in sales you pay five euros in market capitalization. Makes sense if the company is not yet generating stable profits – check the margin.

Dividend yield: Dividend two euros, price 50 euros. Return = 2 / 50 = 4%. Check: Is the dividend covered by free cash flow? If not, the return is deceptive.

ROE: Profit 100 million, equity 500 million ROE = 100 / 500 = 20%. Strong, provided that debt is moderate and equity has not been significantly reduced through buybacks. A high ROE that is based only on a low equity base should be treated with caution.

Operating margin: Operating profit 40 million, sales 200 million. Margin = 40 / 200 = 20%. Increasing margin over several years indicates pricing power and efficiency.

Debt: Net debt 300 million, operating cash flow 150 million. Ratio = 300 / 150 = 2. Solid as long as the business is stable. Cyclical industries need more buffers. Alternatively, you can compare net debt to EBITDA – the logic remains the same.

Cheap or cheap? The reality check

A low ratio does not automatically mean “bargain”. Sometimes the market prices in real problems: shrinking market, weak products, legal risks. Conversely, investors often pay a premium for quality and growth – justified if the company has proven its strength over the years.

So always ask yourself:

- Is the business model robust and understandable?

- Are margins and ROE stable or increasing?

- Does the balance sheet hold up even in difficult times?

- Does the price (P/E/P/S) match the growth and quality?

Only when quality, stability and valuation fit together does an attractive risk-reward ratio emerge. Everything else is speculation.

From the number to the decision: your system

Build a short, written system. It protects you from spontaneous feelings and price fluctuations.

- Define rules: What minimum values do you accept (e.g. positive profits, sustainable debt, stable margin)?

- Choose a standard of comparison: Always compare the industry instead of taking a single look. A software P/E ratio is not comparable to a bank P/E ratio.

- Formulate thesis: Why should the company earn more in three to five years? Name the drivers specifically.

- Price discipline: Set a range within which the ratio of quality to price suits you.

- Review dates: Re-examine every six to twelve months: developments, assumptions, risks.

In this way, key figures become a repeatable process – and uncertainty becomes a decision with substance.

Conclusion

Fundamental analysis is not a jungle of numbers, but a filter. Focus on quality (margin, ROE), stability (earnings, cash flow) and valuation (P/E, P/E) – in the context of the industry. Calculate simple examples yourself, write down your rules and stick to your pricing discipline. This allows you to make calm, understandable decisions, even when the markets are raging. Start today with a company of your choice and go through the 15-minute checklist – the first step creates clarity that you can use in any future analysis.