Rumors have recently been circulating that the Persson founding family could take the H&M share from the stock market through its investment company Ramsbury Invest. The family currently holds around 64 percent of H&M shares and has expanded this share faster this year than in previous years.

A current analysis of BNR Radio shows that the Swedish fashion group faces major challenges despite its global presence and its strong brand awareness. The company, the second largest fast-fashion dealer, is fighting with slow growth, intensive competition and increasing criticism of its sustainability measures. In the BNR-Nieuwsradio-Podcast ‘Doorlicht’, the journalist Nina van analyze the dungs and investment expert Jim Tehupuring H&M so that the listeners can determine whether the stock is suitable for you.

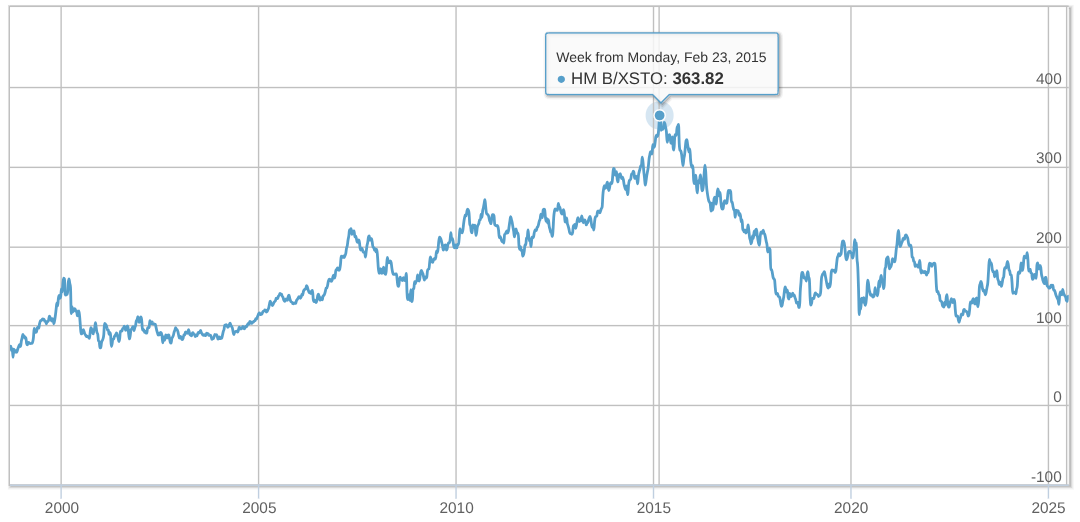

Performance and financial view

H&M’s share price has experienced a significant decline. The stock is traded in around 130 Swedish crowns, a severe decline compared to about 200 Swedish crowns a year ago. The company’s share price has shown a downward or sideways trend in the past ten years and reached a maximum of 363 Swedish crowns in 2015.

Sales have remained relatively stable in recent years and fluctuated between 230 and 250 billion Swedish crowns (20.5 to 22 billion euros).

Despite the stagnating sales, H&M remains profitable annually. The net profit improved from 325 million euros in 2022 to one billion euros in 2024. H&M also offers a dividend yield of around five to six percent, BNR states.

Strengths and weaknesses

H&M enjoys a high brand awareness and a comprehensive global presence with branches in 79 countries and around 140,000 employees: inside. The concept of offering fashionable clothing at affordable prices addresses a broad target group. The company has expanded its offer through cooperation with well -known designers: inside and expansion into segments such as H&M Home and Cosmetics. H&M has a relatively short supply chain that enables him to react quickly to fashion trends. In addition, H&M has a strong online presence, although around 70 percent of sales come from physical business.

The great dependence on physical transactions makes H&M susceptible. A significant weakness is the declining growth, which reached its peak about a decade ago. More than half of the sales of H&M come from Europe. This indicates saturation in these markets and limited opportunities for further geographical expansion.

Opportunities and risks

Opportunities for H&M lie in the expansion to emerging countries such as Southeast Asia and India, where a growing middle class offers significant potential for new customers: inside. The increased sustainability efforts are another important opportunity. Running cost reduction initiatives also offer the option of further optimizing the profit margins.

The biggest threat to H&M is intensive competition from other fast fashion retailers such as Inditex and Primark, which often have faster production cycles. Due to their extremely low prices, which attract younger consumers in particular, new providers such as Temu and Aliexpress are also a significant threat. Increasing costs for production and raw materials in conjunction with increasing occupational safety in low -wage countries also affect profitability. In addition, the changing consumer behavior with a growing preference for vintage and second-hand clothing and a negative perception of fast fashion the business model of H&M.

Compared to competitors such as Inditex and GAP, H&M has developed below average on the stock exchange. Inditex stocks have increased by 90 percent in the past five years and that of GAP by 120 percent, while those of H&M have fallen. Inditex also has higher margins and greater growth, although it is traded with a higher price-profit ratio of 30 compared to 18 for H&M.

For investors: Due to its constant profitability and adequate evaluation, H&M could be attractive as a dividend share, but is not considered a growth share. For investors: In view of the nature of the fast-fashion industry, it is less suitable for investors: The conclusion of BNR radio is less suitable in view of the nature of the fast-fashion industry.

Neither this podcast nor this article provide advice on buying or not buying stocks.

This article was translated into German using a AI tool.

Fashionunited uses AI language tools to accelerate the translation of (news) articles and read the translations correction to improve the end result. This saves our human journalist: inside time that you can use for research and writing your own article. Articles that have been translated using AI are checked and edited by a human editor before the online publication. If you have any questions or comments about this process, send us an email to [email protected]